Impact of Tax Scenarios

The Guinn Center for Policy Priorities has analyzed the impact of the Nevada Revenue Plan approved by the Legislature in SB 483 as well as other proposals considered in 2015 and in prior years. Each figure shows the impact of each tax proposal on a different type of business. For more information, please see our detailed spreadsheets.

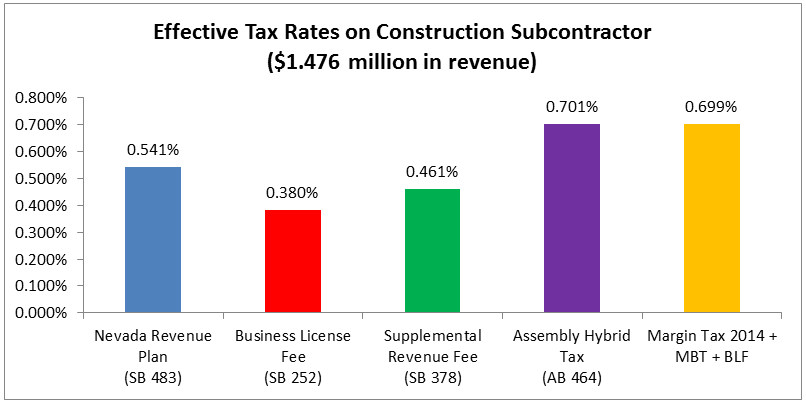

This construction subcontractor relies heavily on human capital. This business has gross receipts of $1,476,000 and $831,000 in payroll costs. Of the 2015 Legislative proposals, the highest effective tax rate would be under the original version of AB 464.

Nevada Revenue Plan (SB 483): As approved by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the construction industry is .083%. The Commerce Tax would not apply to this business since it does not have more than $4 million in revenue. The MBT would also apply. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This would result in a tax of $7,486. In addition, a Business License Fee of $500 for corporations would apply, for a total tax liability of $7,986. This is an effective tax rate of 0.541%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.091% and the amount of the tax is $1,315. A Modified Business Tax (MBT) of $4,300 would also be due based on the current tax rate of 1.17%. The total tax liability would be $5,615, which is an effective tax rate of 0.380%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $6,598. A business license fee of $200 would also be due for a total tax liability of $6,798. This is an effective tax rate of 0.461%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. This would result in a an MBT liability of $9,844. A business license fee of $500 for corporations would also apply for a total liability of $10,344. This is an effective tax rate of 0.701%.

Margin Tax 2014 Proposal: The margin tax proposal of 2014 affected businesses with more than $1 million in gross receipts. A business would take a deduction for cost of goods sold, employee compensation, or 30% of net revenue to calculate the margin. A tax rate of 2 percent would apply to the margin. In this example, the margin is $506,000, which results in a tax of $10,120. A business license fee of $200 would also apply for a total tax liability of $10,320. This is an effective tax rate of 0.699%.

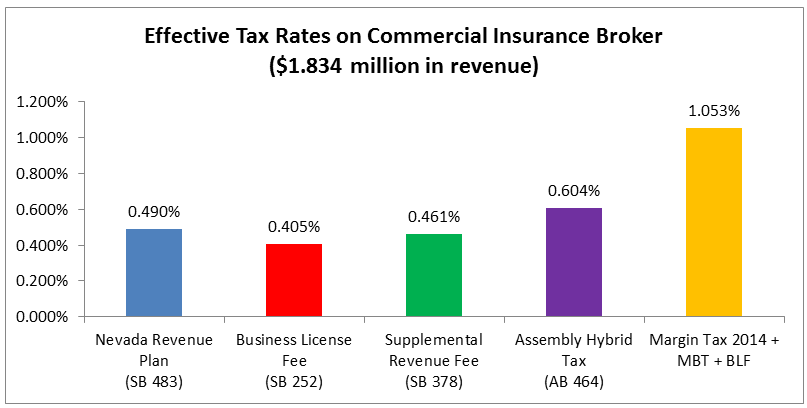

This commercial insurance broker also relies heavily on human capital. This business has gross receipts of $1,834,000 and $878,000 in payroll costs. Of the 2015 Legislative proposals, the highest effective tax rate would be under the original version of AB 464.

Nevada Revenue Plan (SB 483): As adopted by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the insurance industry is 0.111%. The Commerce Tax would not apply to this business since it does not have more than $4 million in revenue. The MBT would also apply. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This would result in a tax of $8,494. In addition, a Business License Fee of $500 for corporations would apply, for a total tax liability of $8,994. This is an effective tax rate of 0.490%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.121% and the amount of the tax is $2,323. A Modified Business Tax (MBT) of $5,100 would also be due based on the current tax rate of 1.17%. The total tax liability would be $7,423, which is an effective tax rate of 0.405%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $8,263. A business license fee of $200 would also be due for a total tax liability of $8,463. This is an effective tax rate of 0.461%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. This would result in a an MBT liability of $10,577. A business license fee of $500 for corporations would also apply for a total liability of $11,077. This is an effective tax rate of 0.604%.

Margin Tax 2014 Proposal: The margin tax proposal of 2014 affected businesses with more than $1 million in gross receipts. A business would take a deduction for cost of goods sold, employee compensation, or 30% of net revenue to calculate the margin. A tax rate of 2 percent would apply to the margin. In this example, the margin is $956,000, which results in a tax of $19,120. A business license fee of $200 would also apply for a total tax liability of $19,320. This is an effective tax rate of 1.053%.

This small medical practitioner is also human capital intensive. This business has gross receipts of $3,790,000 and $1,624,000 in payroll costs. Of the 2015 Legislative proposals, the highest effective tax rate would be under the Business Licensee Fee proposed in SB 252.

Nevada Revenue Plan (SB 483): As adopted by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the health care industry is 0.190%. The Commerce Tax would not apply to this business since it does not have more than $4 million in revenue. The MBT would also apply. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This would result in a tax of $21,004. In addition, a Business License Fee of $500 for corporations would apply, for a total tax liability of $21,504. This is an effective tax rate of 0.567%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.208% and the amount of the tax is $7,982. A Modified Business Tax (MBT) of $15,023 would also be due based on the current tax rate of 1.17%. The total tax liability would be $23,005, which is an effective tax rate of 0.607%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $17,359. A business license fee of $200 would also be due for a total tax liability of $17,559. This is an effective tax rate of 0.463%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. This would result in a an MBT liability of $22,214. A business license fee of $500 for corporations would also apply for a total liability of $22,714. This is an effective tax rate of 0.599%.

Margin Tax 2014 Proposal: The margin tax proposal of 2014 affected businesses with more than $1 million in gross receipts. A business would take a deduction for cost of goods sold, employee compensation, or 30% of net revenue to calculate the margin. A tax rate of 2 percent would apply to the margin. In this example, the margin is $2,166,000, which results in a tax of $43,320. A business license fee of $200 would also apply for a total tax liability of $43,520. This is an effective tax rate of 1.148%.

This automotive and retail sales business conducts a high volume of sales and is not as reliant on human capital as the earlier examples. This business has gross receipts of $31,137,000 and $4,307,000 in payroll costs. Of the 2015 Legislative proposals, the highest effective tax rate would be under the Supplemental Revenue Fee proposed in SB 378.

Nevada Revenue Plan (SB 483): As adopted by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the retail industry is 0.111%. The Commerce Tax would apply to revenue exceeding $4 million, which would result in a tax liability of $30,122. The MBT would also apply. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This would result in a tax of $52,868. Fifty percent of the Commerce Tax Liability ($15,061) would be deducted from the MBT, for a net MBT liability of $37,807. In addition, a Business License Fee of $500 for corporations would apply, for a total tax liability of $68,429. This is an effective tax rate of 0.220%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.121% and the amount of the tax is $37,847. A Modified Business Tax (MBT) of $40,298 would also be due based on the current tax rate of 1.17%. The total tax liability would be $78,145, which is an effective tax rate of 0.251%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $144,522. A business license fee of $200 would also be due for a total tax liability of $144,722. This is an effective tax rate of 0.465%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. This would result in a an MBT liability of $64,069. A business license fee of $500 for corporations would also apply for a total liability of $64,569. This is an effective tax rate of 0.207%.

Margin Tax 2014 Proposal: The margin tax proposal of 2014 affected businesses with more than $1 million in gross receipts. A business would take a deduction for cost of goods sold, employee compensation, or 30% of net revenue to calculate the margin. A tax rate of 2 percent would apply to the margin. In this example, the margin is $11.5 million, which results in a tax of $230,300. A business license fee of $200 would also apply for a total tax liability of $230,500. This is an effective tax rate of 0.740%.

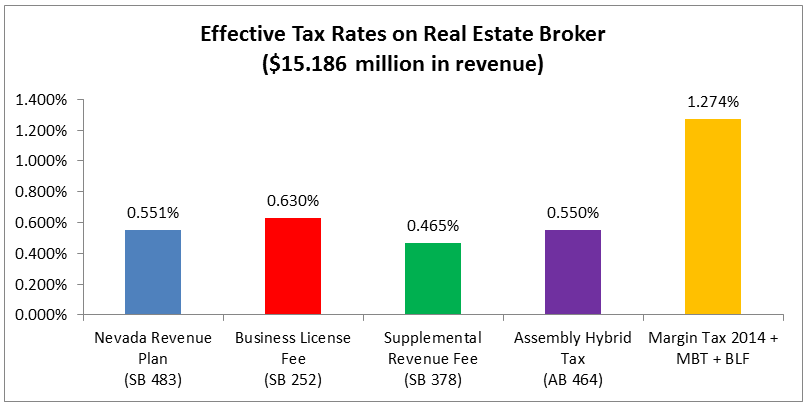

This real estate broker is also an example of a business with high volume sales and low payroll costs. This business has gross receipts of $15,186,000 and $5,526,000 in payroll costs. Of the 2015 Legislative proposals, the highest effective tax rate would be under the Business License Fee proposed in SB 252.

Nevada Revenue Plan (SB 483): As approved by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the real estate industry is 0.250%. The Commerce Tax would apply to revenue exceeding $4 million, which would result in a tax liability of $27,965. The MBT would also apply. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This would result in a tax of $69,257. Fifty percent of the Commerce Tax Liability ($13,983) would be deducted from the MBT, for a net MBT liability of $55,274. In addition, a Business License Fee of $500 for corporations would apply, for a total tax liability of $83,739. This is an effective tax rate of 0.551%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.272% and the amount of the tax is $42,379. A Modified Business Tax (MBT) of $53,298 would also be due based on the current tax rate of 1.17%. The total tax liability would be $95,677, which is an effective tax rate of 0.630%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $70,350. A business license fee of $200 would also be due for a total tax liability of $70,550. This is an effective tax rate of 0.465%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. This would result in a an MBT liability of $83,086. A business license fee of $500 for corporations would also apply for a total liability of $83,586. This is an effective tax rate of 0.550%.

Margin Tax 2014 Proposal: The margin tax proposal of 2014 affected businesses with more than $1 million in gross receipts. A business would take a deduction for cost of goods sold, employee compensation, or 30% of net revenue to calculate the margin. A tax rate of 2 percent would apply to the margin. In this example, the margin is $9.7 million, which results in a tax of $193,200. A business license fee of $200 would also apply for a total tax liability of $193,400. This is an effective tax rate of 1.274%.

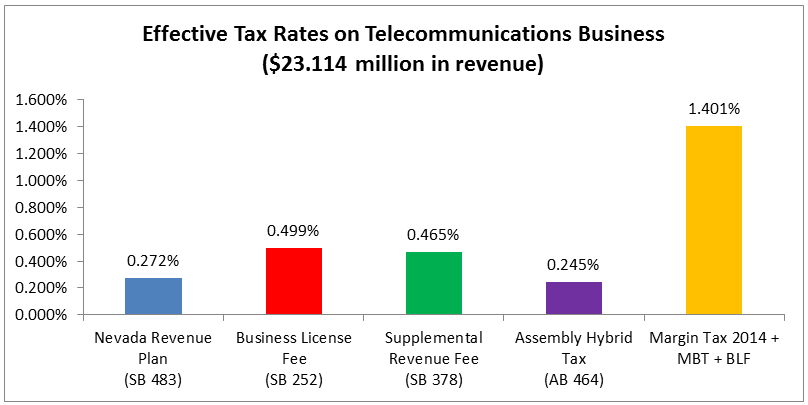

This telecommunications business is also an example of a capital intensive business with low payroll. This business has gross receipts of $23,114,000 and $3,797,331 in payroll costs. Of the 2015 Legislative proposals, the highest effective tax rate would be under the Business License Fee proposed in SB 252.

Nevada Revenue Plan (SB 483): As approved by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the telecommunications industry is 0.136%. The Commerce Tax would apply to revenue exceeding $4 million, which would result in a tax liability of $25,995. The MBT would also apply. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This would result in a tax of $49,308. Fifty percent of the Commerce Tax Liability ($12,998) would be deducted from the MBT, for a net MBT liability of $36,310. In addition, a Business License Fee of $500 for corporations would apply, for a total tax liability of $62,805. This is an effective tax rate of 0.272%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.329% and the amount of the tax is $77,860. A Modified Business Tax (MBT) of $37,474 would also be due based on the current tax rate of 1.17%. The total tax liability would be $115,334, which is an effective tax rate of 0.499%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $107,215. A business license fee of $200 would also be due for a total tax liability of $107,415. This is an effective tax rate of 0.465%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. This would result in a an MBT liability of $56,118. A business license fee of $500 for corporations would also apply for a total liability of $56,618. This is an effective tax rate of 0.245%.

Margin Tax 2014 Proposal: The margin tax proposal of 2014 affected businesses with more than $1 million in gross receipts. A business would take a deduction for cost of goods sold, employee compensation, or 30% of net revenue to calculate the margin. A tax rate of 2 percent would apply to the margin. In this example, the margin is $16.2 million, which results in a tax of $323,596. A business license fee of $200 would also apply for a total tax liability of $323,796. This is an effective tax rate of 1.401%.

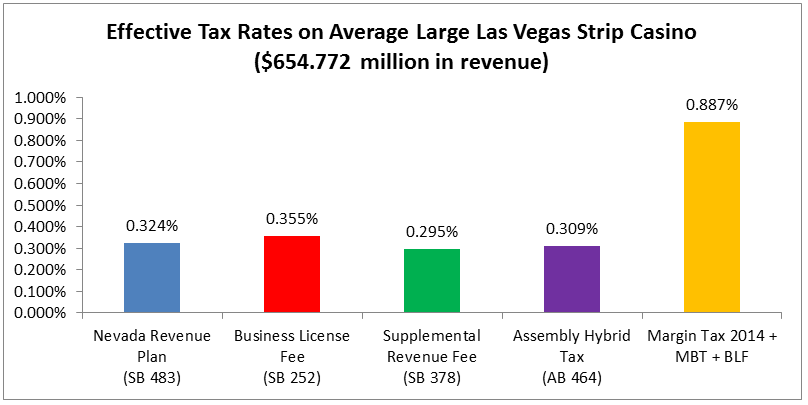

This data represents the average large Las Vegas strip casino. Average gross receipts total $654,772,409 and payroll totals $129,950,156. Of the 2015 Legislative proposals, the highest effective tax rate would be under the Business License Fee proposed in SB 252.

Nevada Revenue Plan (SB 483): As approved by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the accommodations industry is 0.200%. The Commerce Tax would apply to revenue exceeding $4 million, with a deduction for revenue subject to the Gross Gaming Percentage Fee. This would result in a tax liability of $821,861. The MBT would also apply. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This would result in a tax of $1,708,721. Fifty percent of the Commerce Tax Liability ($410,930) would be deducted from the MBT, for a net MBT liability of $1,297,790. In addition, a Business License Fee of $500 for corporations would apply, for a total tax liability of $2,120,151. This is an effective tax rate of 0.324%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.218%. Revenue that is taxed under the Gross Gaming Percentage Fee would be deducted before applying the tax ($239,841,916). After taking this deduction the amount of the tax would be $970,493. A Modified Business Tax (MBT) of $1,353,754 would also be due based on the current tax rate of 1.17%. The total tax liability would be $2,324,247, which is an effective tax rate of 0.355%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue as well as a deduction for revenue taxed under the Gross Gaming Percentage Fee. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $1,929,162. A business license fee of $200 would also be due for a total tax liability of $1,929,362. This is an effective tax rate of 0.295%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. This would result in a an MBT liability of $2,024,102. A business license fee of $500 for corporations would also apply for a total liability of $2,024,602. This is an effective tax rate of 0.309%.

Margin Tax 2014 Proposal: The margin tax proposal of 2014 affected businesses with more than $1 million in gross receipts (excluding gaming revenue). A business would take a deduction for cost of goods sold, employee compensation, or 30% of net revenue to calculate the margin. A tax rate of 2 percent would apply to the margin. In this example, the margin is $$290 million, which results in a tax of $5.8 million. A business license fee of $200 would also apply for a total tax liability of $5.8 million. This is an effective tax rate of 0.887%.

This restaurant has 15 slot machines and has gross receipts of $1,300,000 and $290,000 in payroll costs. Of the 2015 Legislative proposals, the highest effective tax rate would be under the Supplemental Revenue Fee proposed in SB 378.

Nevada Revenue Plan (SB 483): As approved by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the food services industry is 0.194%. The Commerce Tax would not apply to this business since it does not have more than $4 million in revenue. The MBT would also apply. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This would result in a tax of $988. In addition, a Business License Fee of $500 for corporations would apply, for a total tax liability of $1,488. This is an effective tax rate of 0.114%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.218% and the tax is $2,740. There would be no deduction for revenue subject to gaming taxes. A Modified Business Tax (MBT) would also be due based on the current tax rate of 1.17%. This business would have no MBT liability due to its low payroll costs. The total tax liability would be $2,740, which is an effective tax rate of 0.211%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue. There would be no deduction for revenue taxed under gaming taxes. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $5,780. A business license fee of $200 would also be due for a total tax liability of $5,980. This is an effective tax rate of 0.460%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. This would result in a an MBT liability of $1,404. A business license fee of $500 for corporations would also apply for a total liability of $1,904. This is an effective tax rate of 0.146%.

Margin Tax 2014 Proposal: The margin tax proposal of 2014 affected businesses with more than $1 million in gross receipts. A business would take a deduction for cost of goods sold, employee compensation, or 30% of net revenue to calculate the margin. A tax rate of 2 percent would apply to the margin. In this example, the margin is $420,000, which results in a tax of $8,400. A business license fee of $200 would also apply for a total tax liability of $8,600. This is an effective tax rate of 0.662%.

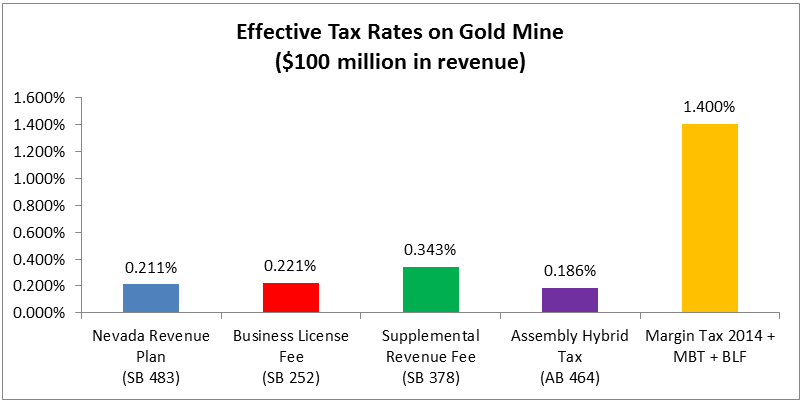

This data represents a large gold mine. Average gross receipts total $100,000,00 and payroll totals $12,069,231. Of the 2015 Legislative proposals, the highest effective tax rate would be under the Supplemental Revenue Fee proposed in SB 378.

Nevada Revenue Plan (SB 483): As approved by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the mining industry is 0.051%. The Commerce Tax would apply to revenue exceeding $4 million, with a deduction for revenue subject to the Net Proceeds of Minerals Tax. This would result in a tax liability of $13,260. The MBT would also apply. For the mining industry, the quarterly deduction would be eliminated and the tax rate would increase from 1.17% to 2.00%. This would result in a tax of $203,970. Fifty percent of the Commerce Tax Liability ($6,630) would be deduced from the MBT, for a net MBT liability of $197,340. In addition, a Business License Fee of $500 for corporations would apply, for a total tax liability of $211,100. This is an effective tax rate of 0.211%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.056%. Revenue that is taxed under the Net Proceeds of Minerals Tax would be deducted before applying the tax ($70,000,000). After taking this deduction the amount of the tax would be $17,389. A Modified Business Tax (MBT) of $197,170 would also be due based on the current tax rate of 1.17%. The total tax liability would be $214,559, which is an effective tax rate of 0.215%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue as well as a deduction for revenue taxed under the Net Proceeds of Minerals. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $139,235. There would also be an MBT of 2 percent for mining businesses, which would be a tax of $203,970. In addition, there would be a business license fee of $200, for a total tax liability of $343,405. This is an effective tax rate of 0.343%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. This would result in a an MBT liability of $185,160. A business license fee of $500 for corporations would also apply for a total liability of $185,660. This is an effective tax rate of 0.186%.

Margin Tax 2014 Proposal: The margin tax proposal of 2014 affected businesses with more than $1 million in gross receipts. A business would take a deduction for cost of goods sold, employee compensation, or 30% of net revenue to calculate the margin. A tax rate of 2 percent would apply to the margin. In this example, the margin is $70 million, which results in a tax of $1.4 million. A business license fee of $200 would also apply for a total tax liability of $1.4 million. This is an effective tax rate of 1.400%.

For the next five figures, we present the impact on a small professional services business at various revenue levels ranging from $200,000 to $1 million. The impact on small businesses varies with each tax proposal. For each small business scenario, the highest effective tax rate of the 2015 Legislative proposals would be under the Supplemental Revenue Fee proposed in SB 378. However, the impact of the other proposals varies based on the size of the small business.

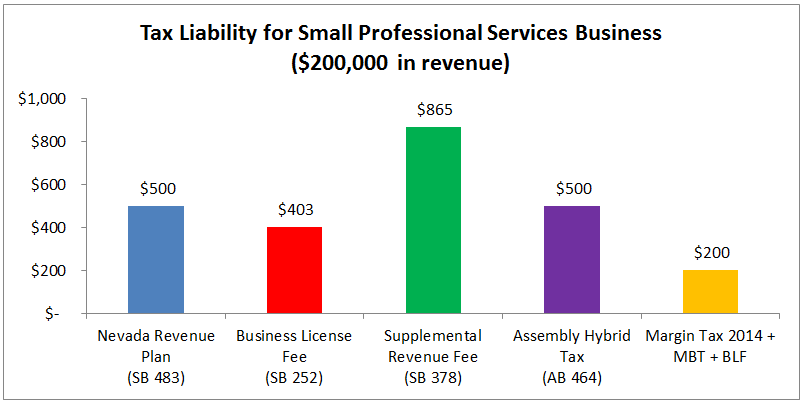

This figure shows a small professional services business with $200,000 in revenue and payroll of $76,000 (38 percent of revenue).

Nevada Revenue Plan (SB 483): As approved by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the professional services industry is 0.181%. The Commerce Tax would not apply to this business since it does not have more than $4 million in revenue. This plan also includes changes to the MBT. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This business would have no MBT liability since quarterly taxable wages are less than $50,000. In addition, a Business License Fee of $500 for corporations would apply, which results in an effective tax rate of 0.250%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.197% and the total tax due would be $403. This is an effective tax rate of 0.202%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $665. There would also be a business license fee of $200, for a total tax liability of $865. This is an effective tax rate of 0.433%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. There would be no MBT liability for this business because annual wages are $76,000 and quarterly taxable wages are only $19,000. A business license fee of $500 for corporations would apply, which results in an effective tax rate of 0.250%

Margin Tax 2014 Proposal: A business of this size would not be subject to the Margin Tax. However, the business would pay the $200 Business License Fee. This is an effective tax rate of 0.100%.

This figure shows a slightly larger professional services business with $300,000 in revenue and payroll of $114,000 (38 percent of revenue).

Nevada Revenue Plan (SB 483): As approved by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the professional services industry is 0.181%. The Commerce Tax would not apply to this business since it does not have more than $4 million in revenue. This plan also includes changes to the MBT. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This business would have no MBT liability since quarterly wages are less than $50,000. In addition, a Business License Fee of $500 for corporations would apply, which results in an effective tax rate of 0.167%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.197% and the total tax due would be $613. This is an effective tax rate of 0.204%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $1,130. There would also be a business license fee of $200, for a total tax liability of $1,330. This is an effective tax rate of 0.443%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. There would be no MBT liability for this business because annual wages are $114,000 and quarterly taxable wages are only $28,500. A business license fee of $500 for corporations would apply, which results in an effective tax rate of 0.167%

Margin Tax 2014 Proposal: A business of this size would not be subject to the Margin Tax. However, the business would pay the $200 Business License Fee. This is an effective tax rate of 0.067%.

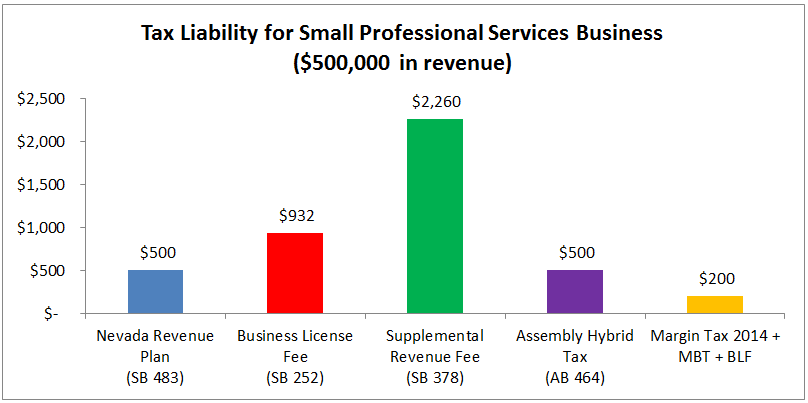

The next example is larger professional services business with $500,000 in revenue and payroll of $190,000 (38 percent of revenue).

Nevada Revenue Plan (SB 483): As approved by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the professional services industry is 0.181%. The Commerce Tax would not apply to this business since it does not have more than $4 million in revenue. This plan also includes changes to the MBT. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This business would have no MBT liability since quarterly taxable wages are less than $50,000. In addition, a Business License Fee of $500 for corporations would apply, which is an effective tax rate of 0.100%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.197% and the total tax due would be $932. This is an effective tax rate of 0.186%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $2,060. There would also be a business license fee of $200, for a total tax liability of $2,260. This is an effective tax rate of 0.452%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. There would be no MBT liability for this business because annual wages are $190,000 and quarterly taxable wages are $47,500. A business license fee of $500 for corporations would apply, which is an effective tax rate of 0.100%

Margin Tax 2014 Proposal: A business of this size would not be subject to the Margin Tax. However, the business would pay the $200 Business License Fee. This is an effective tax rate of 0.040%.

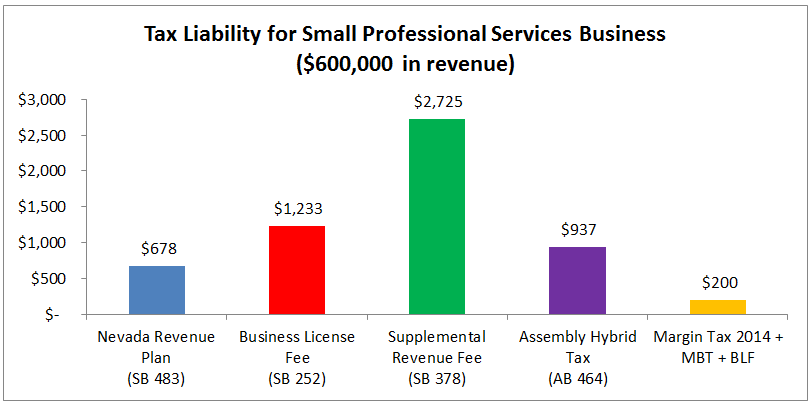

This example reflects a professional services business with $600,000 in revenue and payroll of $228,000 (38 percent of revenue). This example shows how the various proposed changes to the MBT affect a small business that pays sufficient payroll to be taxed under the MBT.

Nevada Revenue Plan (SB 483): As approved by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the professional services industry is 0.181%. The Commerce Tax would not apply to this business since it does not have more than $4 million in revenue. This plan also includes changes to the MBT. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This business would have an MBT liability of $178. In addition, a Business License Fee of $500 for corporations would apply, for a total tax liability of $678. This is an effective tax rate of 0.113%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.197% and the total tax due would be $1,233. This is an effective tax rate of 0.206%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $2,525. There would also be a business license fee of $200, for a total tax liability of $2,725. This is an effective tax rate of 0.454%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. There would be an MBT liability for this business because annual wages are $228,000 and quarterly taxable wages are $57,000. The annual MBT liability would be $437. A business license fee of $500 for corporations would also apply, for a total tax liability of $937. This is an effective tax rate of 0.156%

Margin Tax 2014 Proposal: A business of this size would not be subject to the Margin Tax. However, the business would pay the $200 Business License Fee. This is an effective tax rate of 0.033%.

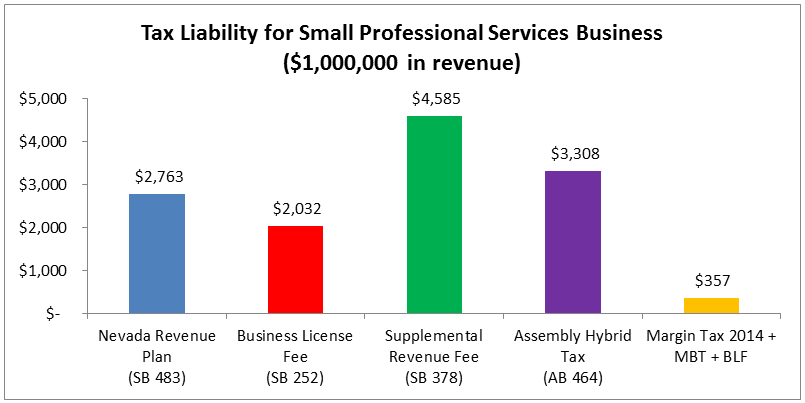

This example shows a professional services business with revenue of $1 million and payroll of $380,000 (38 percent of revenue). This example also shows how the various proposed changes to the MBT affect a small business that pays sufficient payroll to be taxed under the MBT.

Nevada Revenue Plan (SB 483): As approved by the Legislature, a new Commerce Tax applies to businesses with more than $4 million in revenue. The rate for the professional services industry is 0.181%. The Commerce Tax would not apply to this business since it does not have more than $4 million in revenue. This plan also includes changes to the MBT. The quarterly deduction would be reduced from $85,000 to $50,000 and the tax rate would be increased from 1.17% to 1.475%. This business would have an MBT liability of $2,263. In addition, a Business License Fee of $500 for corporations would apply, for a total tax liability of $2,763. This is an effective tax rate of 0.276%.

Business License Fee (SB 252): Under this proposal, the Business License Fee rate for the industry is 0.197% and the total tax due would be $1,875. A Modified Business Tax (MBT) of $157 would also be due based on the current tax rate of 1.17%. The total tax liability would be $2,032, which is an effective tax rate of 0.203%.

Supplemental Revenue Fee (SB 378): Under this proposal, there is a deduction for the first $100,000 in revenue. A Supplemental Revenue Fee is then applied at a tax rate of 0.465% plus $200, for a total tax of $4,385. There would also be a business license fee of $200, for a total tax liability of $4,585. This is an effective tax rate of 0.459%.

Assembly Hybrid Tax (AB 464): Under this proposal, the MBT tax rate would be increased from 1.17% to 1.56% and the health care deduction would be repealed. The bill would also reduce the quarterly deduction from $85,000 to $50,000. There would be an MBT liability for this business because annual wages are $380,000 and quarterly taxable wages are $95,000. The annual MBT liability would be $2,808. A business license fee of $500 for corporations would also apply, for a total tax liability of $3,308. This is an effective tax rate of 0.331%

Margin Tax 2014 Proposal: A business of this size would not be subject to the Margin Tax since that proposal would have applied to businesses with more than $1 million in revenue. However, an MBT of $157 and a $200 Business License Fee would apply, for a total tax of $357. This is an effective tax rate of 0.036%.